CMHC Vancouver Property Market Outlook – Cautious Rebound

The CMHC, Canada’s national housing agency, recently published its Housing Market Outlook. Here’s what they had to say about Metro Vancouver’s property market.

Vancouver’s property market, a perennial source of fascination and anxiety, enters 2025 at a critical juncture. After a period of cooling, the market is poised for a modest resurgence, primarily driven by lower mortgage rates and a renewed vigour in resale activity.

However, this anticipated upswing is tempered by a confluence of headwinds, including cuts in immigration, a torrent of new rental units, and persistent challenges within the condominium sector.

These factors suggest a less exuberant recovery than some might hope, demanding a nuanced understanding of the market's intricate dynamics.

Demand for Existing Homes: A Tentative Thaw

The most immediate catalyst for change is the anticipated rebound in resale activity. Following two years of sluggish sales, the recent easing of mortgage rates is expected to lure buyers back into the market. This renewed interest will likely translate into a modest increase in buyer demand and prices.

However, it's crucial to note that this recovery is projected to be modest, and activity is very unlikely to return to the frenzied peaks witnessed in 2021.

While the impact of recent rate cuts was already impacting late 2024 purchase activity, which exceeded those of the same period in 2023, the overall buyer activist or 2025 is expected to only return to average. This suggests a market cautiously regaining its footing rather than experiencing a dramatic resurgence.

This dynamic is further amplified by the confluence of lower interest rates, pent-up demand from prospective buyers who have been waiting on the sidelines, and the relatively healthy wage growth observed in recent years.

Inventory and Pricing Dynamics: A Delicate Balance

Inventory levels are surprisingly high.

The detached house market is a buyer's market, and buyers have the upper hand in negotiations. Months of inventory increased from 8.4 to 10.8 compared to last year–up 29 percent.

Unlike the detached house market, the apartment market is a balanced market, and buyers and sellers have equal negotiating power. Months of inventory increased from 5 to 6.1 compared to last year–up 22 percent.

The improvement in demand is expected to have a tangible effect on existing inventory levels. Both unsold new homes and active listings, which have been accumulating in recent months, are likely to be absorbed more quickly.

For the first time in years, no new construction projects were launched in January 2025. Demand for pre-sales has gone cold. The CMHC, believes this will change.

Consequently, the average days on the market, a key indicator of market balance, are projected to decline, potentially placing upward pressure on prices.

A return of price growth, even if modest, is also expected to reignite interest from investors, particularly those seeking opportunities in the presale market.

Migration and Housing Demand: A Shifting Landscape

Despite the positive signs in the resale market, the broader picture is complicated by evolving migration patterns.

RBC: The federal government’s plans to reduce new arrivals are expected to essentially wipe out all previously expected population growth in years ahead. While the final impact on population is yet to be known, the direction will be lower, turning demographics from a tailwind to a headwind. link

Changes in international migration policies, while having a less direct impact on the resale market compared to the rental sector, will nonetheless be felt in Vancouver, a favoured destination for many new arrivals. Slower population growth, driven by adjustments to immigration targets and ongoing interprovincial migration, will exert a dampening effect on overall housing demand. This demographic shift presents a significant challenge to the market's long-term growth prospects.

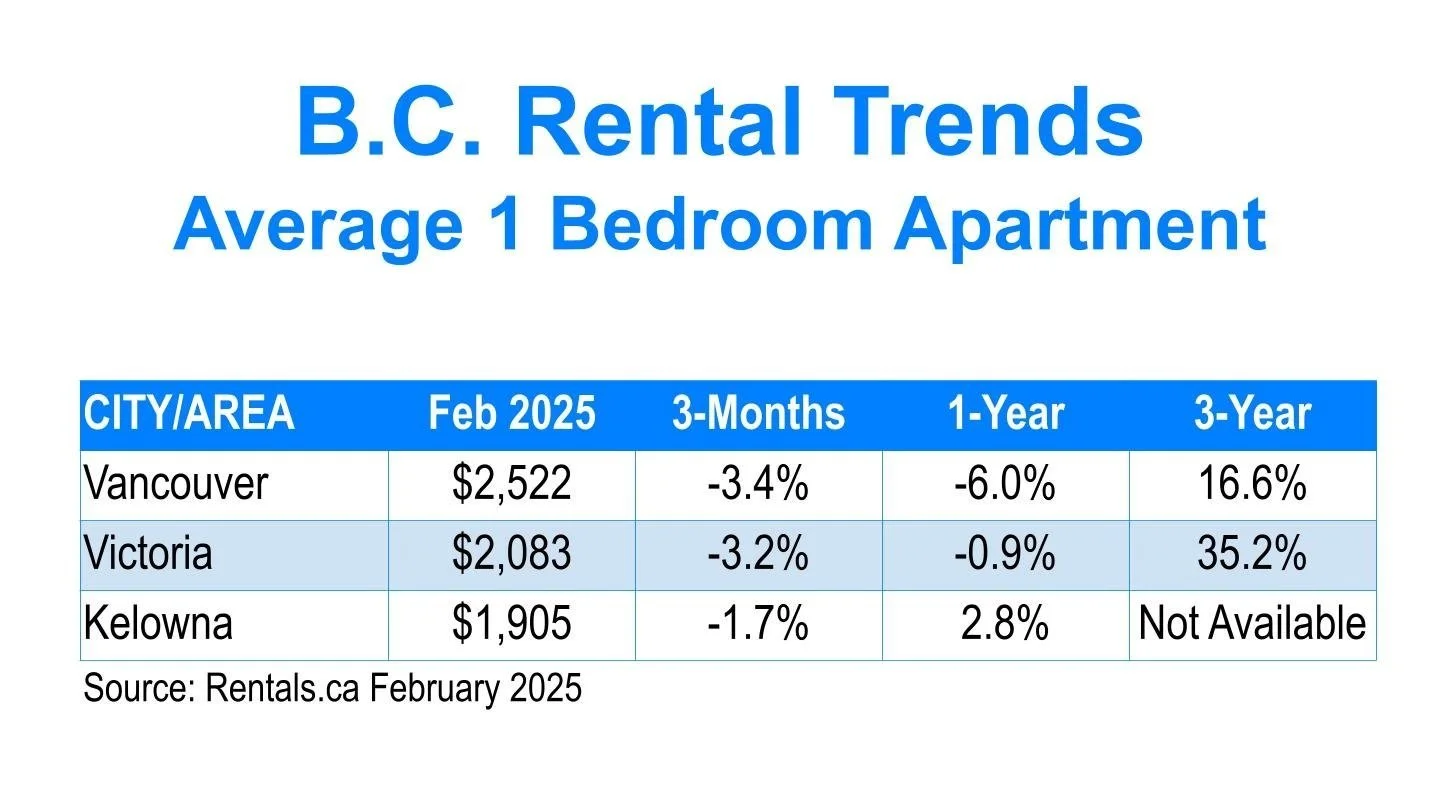

In the CMHC’s December 2024 Rental Market Survey, Metro Vancouver’s rental vacancy rate was 1.6%, while 3 to 5% is considered a ‘normal’ vacancy rate. So, the rental supply is tight, and still rent rates have started to slide regardless.

It’s difficult to reconcile the CMHC’s statement, “The return of price growth in 2025 will also help spur expectations for investors, especially those looking at presales.”

When they also said, “Investors who bought pre-construction units to rent out are increasingly selling as costs rise faster than rental incomes.”

In addition, population growth is expected to go reverse.

Would investors buy rentals that don’t cover their costs, with a risk of rents falling further, in the hopes of recovering the up-front transaction costs and operating losses when prices eventually rise?

New Home Construction: Navigating a Complex Terrain

The new home construction sector presents a complex and somewhat contradictory picture. Housing starts are projected to experience a marginal increase in 2025, primarily driven by multi-unit rental projects.

Condominium Market Challenges: Lingering Concerns

The condominium market continues to face unique challenges. While a stronger resale market will undoubtedly provide some support, lingering concerns about pricing and a persistent lack of robust presale activity continue to plague the sector.

Rising unabsorbed inventory, coupled with the muted price growth observed recently, has delayed some projects.

Although lower mortgage rates may entice some buyers, a scarcity of suitable land for development in recent quarters could further constrain multi-unit construction. This combination of factors suggests a condominium market struggling to find its footing.

Rental Market Vulnerability: A Looming Oversupply

Perhaps the most vulnerable segment of the market is the rental sector. Vacancy rates, which began climbing in 2024, are expected to remain elevated for the foreseeable future. A record number of new rental units are currently under construction and poised to flood the market.

This surge in supply, combined with slower population growth and reduced immigration, is likely to exert downward pressure on rents, even as average rents continue to rise due to the influx of new, higher-priced units. This increased competition among landlords could ultimately benefit tenants, potentially leading to improved affordability and higher tenant turnover as the gap between rents for occupied and vacant units narrows.

Conclusion: A Balancing Act

Vancouver's property market in 2025, is navigating a delicate balancing act. While lower mortgage rates and an expected resurgence in buyer activity offer a glimmer of hope, the market faces various challenges.

Shifting migration patterns, a potential glut of new rental units, and persistent concerns in the condominium market suggest that the recovery will be gradual and uneven.

As always, Vancouver's property puzzle remains complex, with its ultimate path dependent on a delicate interplay of economic forces, demographic trends, policy decisions, and the ever-shifting market sentiment.