Mortgage Rate Forecast to 2023

HIGHLIGHTS

|

Every economist surveyed expects the Bank of Canada (BoC) will keep its ‘Target Rate’ at the ‘effective lower bound’ of 0.25% until the second half of 2022. Royal Bank is the only forecaster calling for a rise in the Target Rate by September 2022.

The Bank of Canada will keep interest rates low until the economy has recovered and inflation has reached roughly 2 percent.

While low rates help borrowers, the expectation of prolonged lower interest rates indicates that the economy will likely not fully recover until late 2022.

The first COVID-19 vaccine shipments arrived in Canada on December 13th. The federal government has coordinated the provincial vaccination strategies and has planed for “every Canadian" who wants to be vaccinated to get the shot "by September."

Since Coronavirus has caused such a sharp economic contraction, we expect a robust economic bounce-back as soon as the Pandemic clears. In other words, the economy will have shrunk so much that it will be easy to improve on the dismal past performance.

This article will explain the forecasts for variable (floating) rates and 5-year fixed (locked-in) rates. Keep reading to learn what the big banks are saying about rates.

THE CURRENT SITUATION

Record-low Mortgage Rates

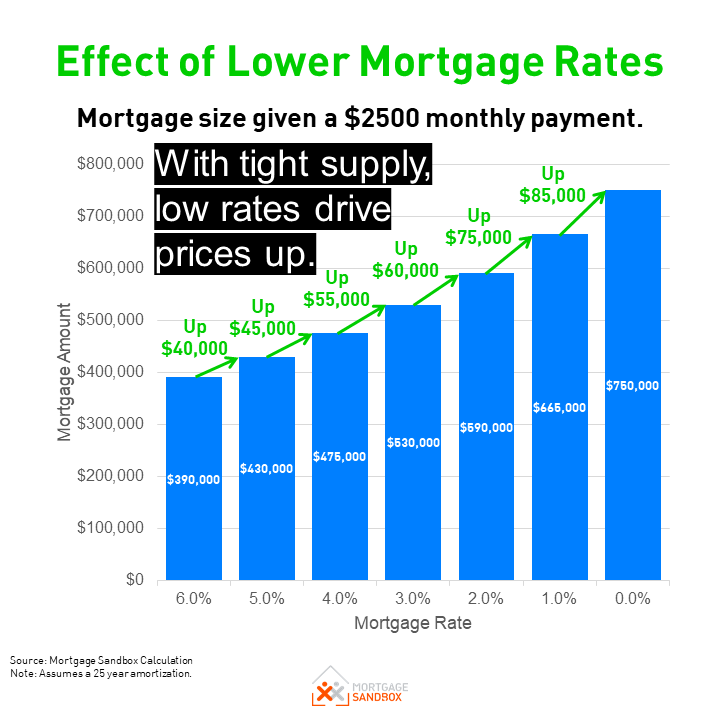

Fixed-rates are currently setting record lows, which is one reason why home prices are rising during a recession.

Low Rates Can Drive-Up House Prices

As rates drop, the impact on homebuying budgets grows stronger.

If there is ample housing supply and the price of a ‘standard home’ remains the same, a low rate allows people to buy more spacious or luxurious homes.

In markets that are short supply, it merely provides homebuyers with more financing so they can bid up the price of a ‘standard home.’

So lower rates alone do not improve housing affordability in the long run.

MORTGAGE RATE FORECASTS

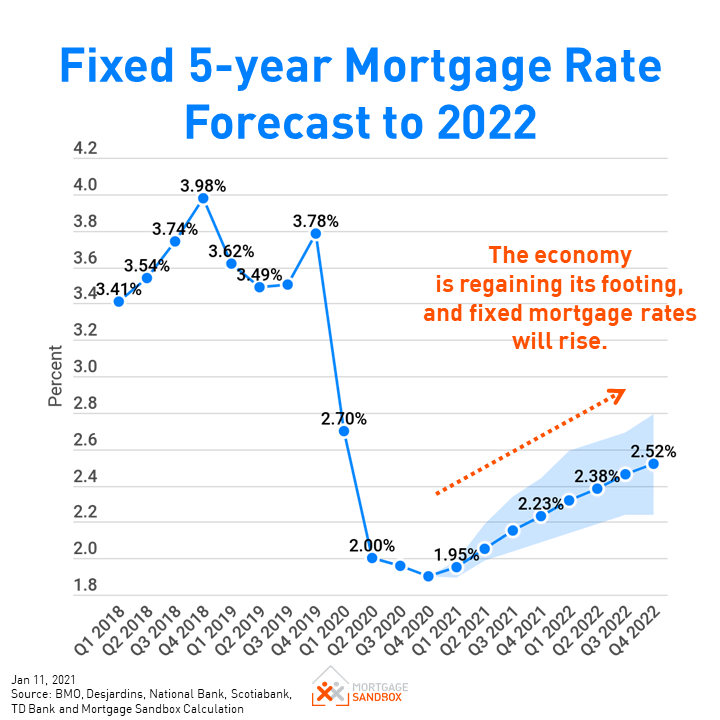

Should I Lock in a 5-Year Fixed Rate?

Banks charge extra interest for the privilege of borrowing at a fixed rate. Usually, they charge more the longer the rate is locked-in. Is it worth paying extra for their fixed-rate service?

Locking in a 2.00% 5-year fixed mortgage rate will only start benefiting you financially if variable rates begin to climb.

Variable rates are not expected to rise until late 2023, so it’s almost a fifty-fifty coin toss.

If you lock in a 5-year rate today, you might be paying slightly more interest for three of the five years. Locking-in is only worth it if variable rates rise by 1% for the final two years of the mortgage term and no one is forecasting rates as far out at 2026

I have a variable rate today. Should I lock in now or wait?

Most variable-rate mortgages allow you to lock-in anytime. Should you? If you want the security of a locked-in rate, locking-in now seems prudent. Fixed-rates are not expected to drop further.

In 6 months, fixed rates will probably be the same or slightly higher than today.

Fixed-rates Provide Peace of Mind

If the risk of rates rising worries you, then you should consider a fixed-rate mortgage rate term. Locking in your rate provides peace of mind, but it does come with some risks that many people aren’t aware of.

Fixed-rates Have Higher Cancellation Penalties

Suppose you are planning to sell or move in the next few years. In that case, cancelling a fixed-rate mortgage before completing the full term can result in a significant penalty fee.

Shall I Get A Variable Rate Mortgage?

Variable rates are typically a little lower than fixed-rates because the borrower takes on the risk of rates changing over time.

Variable rates are expected to remain low for the foreseeable future. Of the economic forecasters that we watch, only Royal Bank expects variable rates to rise in 2023.

How much can I afford?

Try our homebuying budget calculator

HOW FORECASTS WORK

Forecasts are built on assumptions, so naturally, different assumptions about what will happen lead to different forecast results. That is why Mortgage Sandbox publishes the range of projections and the average of all the forecasted rates.

Apart from the economic assumptions, there is also guidance from the Bank of Canada. The Bank interferes in markets to push rates below the level that the free market would set. Often, Bank guidance is more important than the economic fundamentals when it comes to rates.

Forecast Assumptions

A Weak Economy

Canada is now in a recession. Recently, most reports have been adjusting expectations downward as a result of a wave 2 of infections.

In other words, past predictions underestimated the economic impact of prolonged Coronavirus containment efforts. Assuming the vaccination program will not be complete until September 2021, Canadians should prepare themselves emotionally for a third wave.

Bank of Canada Guidance

The Bank of Canada has said that it will hold the policy interest rate at 0.25% until the economy recovers and inflation reaches a consistent 2 percent. Inflation has never consistently reached 2% since the 2008 financial crisis.

In January, the Bank of Canada said that it projects inflation will not reach 2% until sometime in 2023.

Long-term, the Bank of Canada will work toward raising rates to the ‘neutral range’.

The Bank Rate is well below what would be considered a neutral range. According to the Bank of Canada, "Governing Council continues to judge that the policy interest rate will need to rise over time into a neutral range to achieve the inflation target." This policy implies that once Canada emerges from a recession, rates will begin to rise.

Read: Why is the Bank of Canada increasing your borrowing costs?

Forecast Foundations

Fixed-Rate Mortgage

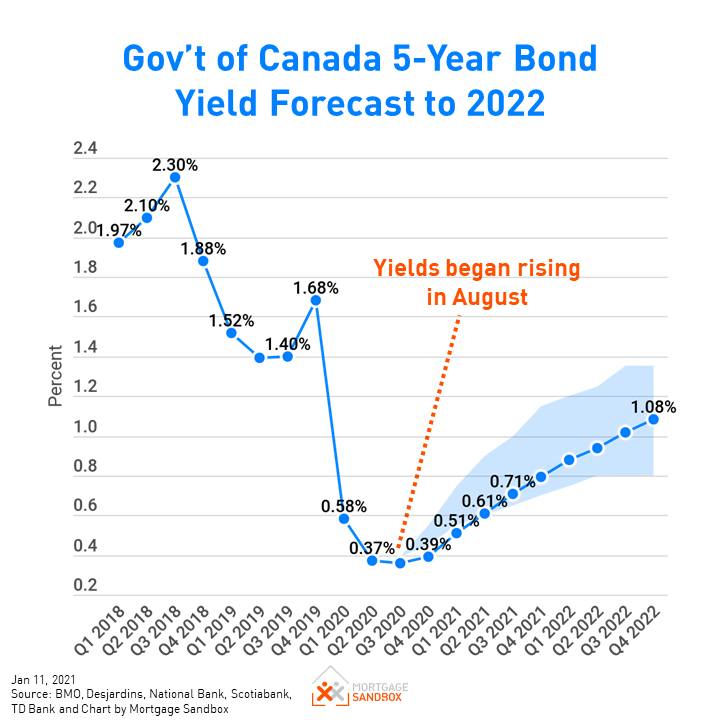

The foundation for a 5-year fixed-rate mortgage forecast is the five-year government of Canada bond, and the government is considered a riskless borrower.

Mortgage loans are considered low risk but riskier than loans to the government. So the average Canadian has to pay 1.5 to 2 percent more on a mortgage than the government pays to borrow money. The spread or gap between the government borrowing rate and another loan rate is called a ‘risk premium’.

Variable-Rate Mortgage

The foundation for a variable-rate mortgage forecast is the Bank of Canada ‘target rate’.

The average Canadian also pays a risk premium above the target rate when they get a variable rate mortgage. The target rate and variable mortgage rates don’t move in perfect synchronization, but they usually trend together.

Sources

We’ve surveyed the largest Canadian banks and their forecasts to develop our analysis.

KEY TAKEAWAYS

Our advice is to speak to a Mortgage Broker as early as possible to lock in a rate. You can lock in your mortgage rate up to 120 days before closing on a home purchase or the renewal of your mortgage.

Here’s our mortgage renewal guide that will help you navigate the process.

Is it a better time to Buy or Sell a home?

There are more economic factors on balance, putting downward pressure on home prices than upward pressure. However, that was also the case in the second half of 2020 when low rates and buyer sentiment carried home values higher.

The link between home prices and economics seems to have weakened. If we believe that home prices are related to the economy's strength, then prices may have peaked for this economic real estate cycle.

If we believe that interest rates are the primary driver of home prices, then the forecasted rise in rates would indicate prices will moderate in the second half of 2021.

Population growth is also expected to remain below average in 2021.

Homebuyer Advice

If you plan to buy in the next three years, be mindful that there is a risk that prices will fall in the short-run, so a ‘wait-and-see’ approach may be appropriate.

For buyers who are still employed, the low mortgage rates provide more purchasing power. In a weakened market, that is a gift to homebuyers; however, it inflates the value of a ‘standard home’ in a market with low supply.

Home Seller Advice

If you were planning to sell, then it may be worthwhile selling sooner than later.

If we use the Great Recession as a guide, it could take between two and ten years for home prices to recapture current highs.

Like this report? Like us on Facebook.